By Sarah Gantz

The Baltimore Sun

WWR Article Summary (tl;dr) Founded in 2005 as a way to spur growth in developing countries, Kiva has expanded to more than a dozen American cities. In Baltimore, Kiva’s model is designed to offer loan opportunities to people whose low credit scores, debt or other financial shortcomings have prevented them from being approved for other financing. Its loans range from $500 to $10,000 and are funded through its crowdsourcing website.

The Baltimore Sun

Kiva, a nonprofit microlender, is expanding to Baltimore with a three-year goal of making 700 loans to entrepreneurs and small business owners who have been turned down for traditional financing, such as a business loan or line of credit.

Founded in 2005 as a way to spur growth in developing countries, Kiva has expanded in recent years to more than a dozen American cities, where leaders see an opportunity to use the same model to help residents in low-income areas lift themselves up.

“We see ourselves as the first rung on the ladder to capital access,” said Adam Kirk, digital marketing manager for Kiva U.S. “Maybe you have a damaged credit score — Kiva is willing to give you a shot. You can borrow with us and build your credit back.”

In Baltimore, Kiva will work with Guidewell Financial Solutions, a Catonsville-based financial counseling organization, to target women and minority entrepreneurs.

Guidewell works in low-income neighborhoods to help residents with debt management, financial literacy and credit counseling. The referral agreement with Kiva is a way to expand Guidewell’s offerings to include micro-loans and maintain contact with clients who otherwise might have been lost after being referred to another organization, said Tom Simonton, director of housing and community development for Guidewell.

In return, Guidewell offers Kiva a recognizable local brand and insight into the city’s business community as the lender tries to break into the Baltimore market. Kiva seeks out organizations like Guidewell, which it calls “trustee partners,” to help anchor it in every city it expands to.

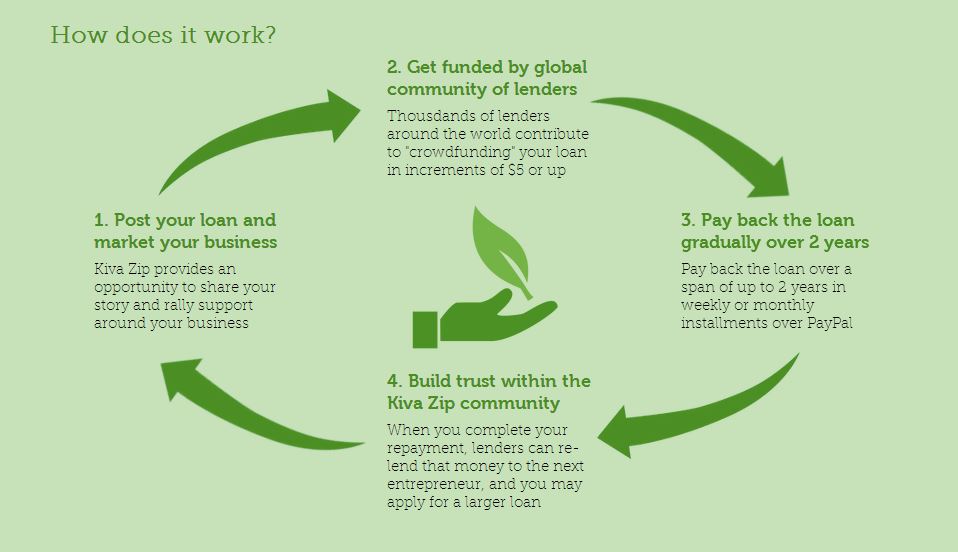

Kiva’s model is designed to offer loan opportunities to people whose low credit scores, debt or other financial shortcomings have prevented them from being approved for other financing.

Its loans range from $500 to $10,000 and are funded through its crowdsourcing website. Donors from around the world commit at least $25 to projects and get their money back as borrowers pay off their loans, typically over 36 months. If borrowers don’t raise money to support the loan through crowdfunding within 30 days, they do not get the loan and lenders get their money back.

The company claims a 97 percent repayment rate for investors. Kiva balances the risk of taking on individuals with less desirable credit by investing in those who can prove they are committed to their business idea and to their community.

Before the loan is opened to public investing, applicants must bring in a certain number of their own investors — often friends or family members — to demonstrate their commitment.

“We are trying to get at borrowers’ strength of character and character in the community,” said Jonny Price, senior director of Kiva U.S.

As one of its first loans in Baltimore, Kiva has approved a $10,000 loan for Deborah M. Cooper, the chef-owner of Debbie’s Cuisine Catering in Baltimore. So far, she has raised $1,100 toward the loan and had 27 days remaining to raise the rest as of Monday.

Cooper launched her small catering business in 2013 and cooks meals for an organization that serves individuals with disabilities.

The loan would pay for new equipment and hiring more workers as Cooper prepares to take on a second contract, serving meals to an additional 95 individuals with disabilities, in October.

Cooper was rejected for a line of credit because, she said, of financial hardship following her divorce, which came around the same time she quit an accounting job to pursue culinary school.

The loan approval from Kiva was an important step, she said.

“It was refreshing,” Cooper said. “It was another notch that said, ‘Hang in there, Debbie. Don’t give up.'”

Microfinancing was made popular by the Nobel Prize-winning Grameen Bank in Bangladesh, developed by economist Muhammad Yunus in the 1970s. The bank, and other microfinance institutions that followed, give credit to people with no or little collateral as a way to stimulate long-term economic growth.

The model is becoming more popular in developed countries and has great potential in cities like Baltimore, where there is a demand for jobs and where poverty may be a barrier to small business ownership, said Peter Lorenzi, a management professor at Loyola University of Maryland.

“The philosophy of microfinance was to fund people who were poor, marginalized or lacked opportunity to regular financial services,” he said. “That describes Baltimore probably better than most American cities.”

Lorenzi has invested in at least 400 businesses through Kiva since learning about the organization years ago and said he is eager to see what promising projects emerge in Baltimore.