By Tracey Lien

Los Angeles Times.

OAKLAND

Mobile apps are often hailed as a solution to many of life’s most mundane problems. Need to order a pizza? Hail a ride? Get someone to do your laundry?

But when it comes to the social and economic problems that plague millions of Americans, the app world hasn’t been as quick to offer help.

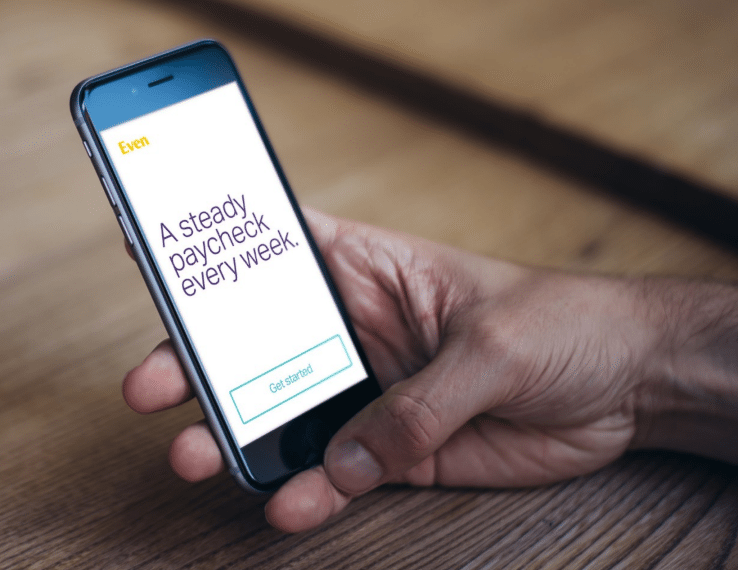

One company, Even, is bucking the trend of flapping birds and candy waiting to be crushed by creating an app that aims to improve the lives of some of America’s least-privileged. Its mission: to solve income volatility.

Millions of Americans who freelance or work hourly jobs experience income fluctuations: They don’t know how many hours they’ll work each week, and they don’t know how much they’ll get paid. They include fast-food workers, nail salon technicians, maids, gardeners and retail employees.

The Even app, currently by invitation-only, eases users’ income volatility by stabilizing their take-home pay. That goes a step further than the slew of budgeting apps out there that simply show users how much money they have and how much they should spend and save.

Here’s how it works: The app connects to people’s bank accounts and sees when the person is paid. It then calculates an average for what the person would be paid if his or her income were stable, and pays them that amount each payday.

If a person gets paid less than the calculated average, Even automatically boosts his or her pay by giving an interest-free advance. If a person gets paid more than the average, Even puts aside that bonus cash to pay back past advances and for future advances.

Even plans on reaching those who need the service the most by partnering with companies with hourly workers. Although no partnerships have been announced yet, a service like Even could benefit workers at companies like Starbucks, Best Buy and Whole Foods, with the promise of reducing worker attrition caused by financial stress, co-founder Jon Schlossberg said.

The Oakland company currently charges users $3 a week for the service, which can be suspended at any time.

If it sounds like the company is taking on a big risk, that’s because it is. One of the biggest challenges the company will face is when a user loses his or her job or is unable to pay back the advances.

Jake Fuentes, founder and chief executive of budgeting app Level Money, said Even could play an important role in filling a market niche, but it may find itself in the difficult position of having to cut people off if they’re deemed too risky a customer.

The founders are aware of these potential hurdles. Even isn’t a bank. It doesn’t dole out loans or charge interest. It makes money when customers subscribe to the service but don’t need Even’s advances.

Schlossberg acknowledged that the business model may not immediately look profitable when compared with payday loan companies, which make money off charging people interest when they are in financially desperate situations.

“But with a mission like this, I ask you: Because we might fail, does that mean we should not try?” Schlossberg said when the service was first announced in January.

Schlossberg is particularly determined to make Even work because he sees it as a solution to a problem that he said he’s been fascinated by since he was a teenager. He recalls watching “Cops” when he was 16 and noticing the same perpetrator in two separate episodes.

“That was remarkable to me,” he said. “Appearing on ‘Cops’ once is bad enough because it means you’ve made some bad decisions. But to be on ‘Cops’ more than once, you have to be seriously making some bad decisions in your life. That was just unfathomable to me.”

So began what he described as a “casual obsession” with finding out why people make objectively bad decisions, and what can be done about it.

His research pointed him to an area of neuropsychology that looked at the effect of poverty on cognitive function. Dozens of scientific journals have detailed how the stress of living in poverty can affect brain chemistry, which can lead people to make poor decisions.

Schlossberg and his fellow Even co-founders Ryan Gomba, Cem Kent and Quinten Farmer saw an opportunity to do for poverty what Silicon Valley entrepreneurs have tried to do in any field they’ve entered: cause disruption.

A 2015 report by the Economic Policy Institute found that more than 30% of working Americans experience significant spikes and dips in their incomes, and the lowest income workers tend to be the most adversely affected. A report published by the JPMorgan Chase Institute this year called on government and corporations to develop tools that could help people manage their bottom line.

Other tech companies are also stepping up.

Mint is one such app that has risen to the occasion, helping customers track their spending. Level Money recently updated its app to detect nuances in transactions and help people budget for bills, loan repayments and other recurring expenses. Even gets more involved by managing people’s money for them.

The app is already seeing results among the small group of hourly wage workers who received early access to the service. The company says people whose take-home pay was once tied to unpredictable work schedules or client numbers have reported feeling less stressed and being better able to plan their spending and loan repayments.

“I feel like I have more security behind me,” Heather Jacobs, 28, a massage therapist whose pay is determined by how many clients she massages in a day, said in a video the company put together. “I’m not stressing completely over paychecks anymore.”

But even if the company offers a compelling solution to income volatility, it still faces hurdles, said Ariel Michaeli, chief executive of analytics firm AppFigure.

“It’s an intriguing idea, but for them, the challenge is going to be how do they sell this kind of concept?” Michaeli said. “How do you educate the market and get everyone to use it? For them, it’s all about the big numbers, and they have to hit a critical mass. It could be an uphill battle.”

There’s also an existential problem: If Even succeeds, isn’t it helping its customers not need a service like Even down the line?

“That’s a valid point,” Schlossberg said. “What that means is as a business we need to offer more products that are valuable to people when they achieve the next level.”