By David Ng And Ryan Faughnder

Los Angeles Times

WWR Article Summary (tl;dr) “The deal for an investor group to acquire Harvey Weinstein’s former movie and TV studio has collapsed in yet another twist in an ongoing saga that has seen agreements come and go amid the general chaos surrounding Weinstein Co.”

Los Angeles Times

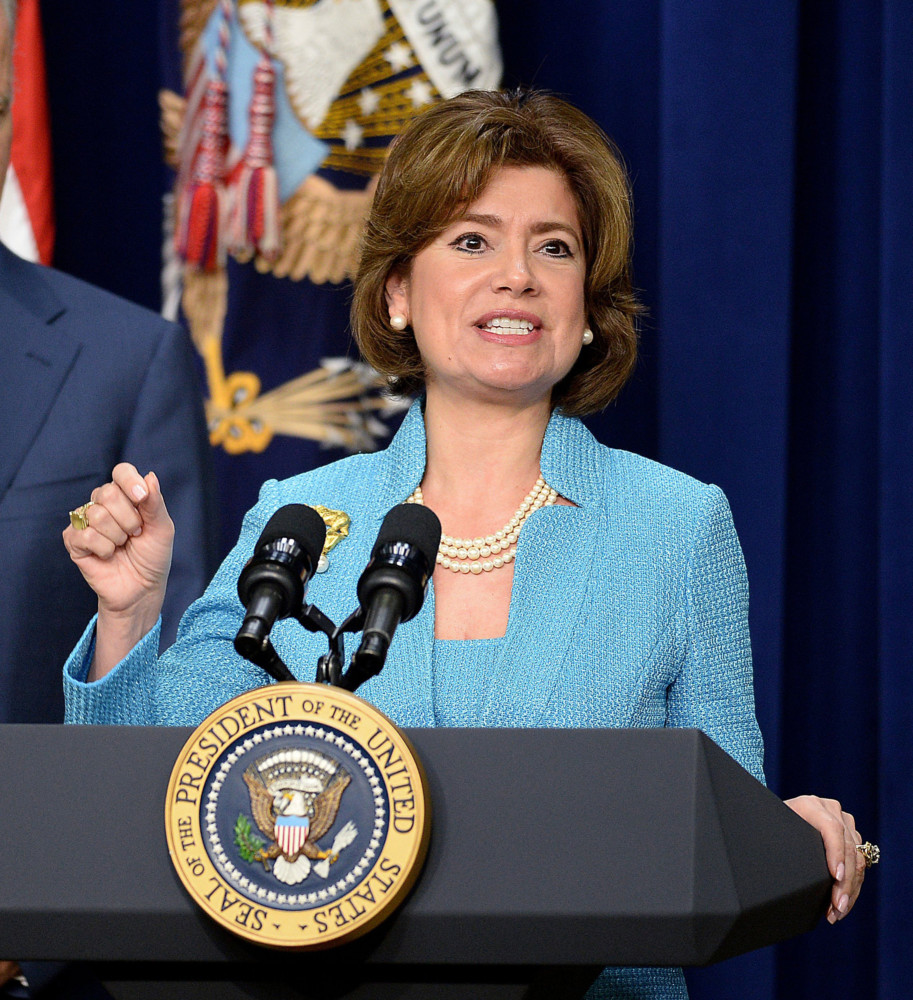

A source close to Maria Contreras-Sweet, a former Obama administration official who is leading the investment group, said Tuesday that there was about $50 million more debt on the New York company’s books than previously thought.

“All of us have worked in earnest on the transaction to purchase the assets of the Weinstein Company. However, after signing and entering into the confirmatory diligence phase, we have received disappointing information about the viability of completing this transaction,” Contreras-Sweet said in a statement.

“As a result, we have decided to terminate this transaction.”

The latest development increases the likelihood that Weinstein Co. will file for bankruptcy protection and casts additional uncertainty over the fate of the company’s estimated 130 employees in New York and Los Angeles.

Harvey Weinstein was forced out of the company he co-founded after dozens of women accused him of sexual misconduct.

Contreras-Sweet’s group, backed by billionaire Ron Burkle, had announced Thursday that it had reached an agreement in principle to buy Weinstein Co., subject to a 40-day closing period.

The terms of the agreement weren’t disclosed, but The Times learned that the bid was worth $500 million, including the assumption of $225 million in debt. The agreement was reached after a last-minute meeting between the investor group and Weinstein Co.’s board of directors at the office of New York Atty. Gen. Eric Schneiderman, who had criticized the planned sale last month. His office had sued the company, saying any deal would have to adequately compensate victims, protect future employees and not enrich people he said were complicit in Weinstein’s alleged abuses.

The bidders took some steps to address Schneiderman’s concerns, including promising to set aside a $90-million fund to compensate Weinstein’s accusers.

But another key stumbling block emerged in recent days.

A source familiar with the deal said the buyers recently discovered undisclosed liabilities, including $27 million in residuals and profit participation and $20 million in accounts payable. There was also a $17-million debt outstanding in connection with a commercial arbitration award.

Contreras-Sweet said Tuesday that the group will consider acquiring Weinstein Co. assets that may become available in the event of bankruptcy proceedings.

The abandoned deal would have put a female face on a company that has been besieged by the sexual harassment and assault accusations against Harvey Weinstein. The bidders had vowed to install a mainly female board of directors and rebrand a studio badly tarnished by the allegations against its co-founder.

Weinstein has denied all allegations of nonconsensual sex.

“I remain committed to working to advance women’s business ownership in all sectors and to inspire girls to envision their futures as leaders of important companies,” Contreras-Sweet said in her statement.

A spokeswoman for the New York attorney general’s office said in a separate statement Tuesday: “We’ll be disappointed if the parties cannot work out their differences and close the deal. Our lawsuit against the Weinstein Company, Bob Weinstein, and Harvey Weinstein remains active and our investigation is ongoing.”

Contreras-Sweet’s offer for the company, which first came to light in November, represented a surprise chance for survival for the studio.

Bids came due in late December. Santa Monica studio Lionsgate, known for “La La Land” and “The Hunger Games,” was interested in buying certain assets of the company. Killer Content, the New York production company behind “Carol” and “Still Alice,” had offered to buy the assets and remake them into an entity to support women. Other bidders included Miramax (owned by BeIN Media) and private equity firms Shamrock Capital Advisors and Vine Alternative Investments.